If you enjoy this newsletter and want to support my writing, consider becoming a paid subscriber ❤️

My new favorite question to ask people is:

What’s new with your finances?

It really makes their eyes dance.

But every single person I asked this question to - from my college bestie to someone I was sitting next to at my coworking space — had an answer within 5 seconds.

None of their answers were: nothing

My college bestie vented that her finances took a hit when her accountant told her that she owed a whopping $10k in taxes.

The coworking stranger admitted that he’s still recovering, two years later, from putting too much of his disposable income into the NFT craze.

I even asked my dentist and he rambled on and on about a backdoor Roth IRA as he was pushing a metal took into my gum line. It made me regret not only the question but also my own existence in his chair.

It’s such a good question because it gets people to open up and talk about something so stupidly hush hush: money.

I’m guilty of this too.

I’ll tell you absolutely everything about my life. I’ve been writing about it for a decade on the internet. But if you ask me how much money I make every year, I’ll point to the sky and say: look! a bird! and run into the nearest Starbucks. I don’t know why that question creeps me out.

👋Welcome to the Monday Pick-Me-Up. I’ll happily show you pictures of my placenta instead of just answering the freaking question about how much money I make. But today, I’m diving deep into my finances (from how much I pay in rent to how I manage my money) and giving you access to it all. My hope is that this either inspires you to write out the details of your own money journey so you spot mistakes or set goals or it just makes you feel more comfy having a convo about money with someone you love or someone you just met at in line at the airport bathroom.

Background information:

I’m 36 and I live in Brooklyn. I’m married, have a dog, and a baby. We live in a one bedroom apartment that we rent. We don’t own anything (ex: house, car, property, etc.). Neither of us have any debt.

Adam and I keep our finances separate. Once we had a baby, we decided to have one joint checking account and credit card.

We contribute the same amount to the joint checking account every month. It’s enough to cover our recurring monthly costs (rent, insurance, etc.) and the joint credit card bill (Gemma/Goofy stuff, groceries, household items).

Other than that, our finances are split. I use my credit card for whatever I want and pay it off every month. I never, ever, keep a balance on it. I also handle all my own investments and retirement contributions. He does the same for his money.

I remember telling a friend of mine that Adam and I keep our money separate and she said: oh, no, what a bad idea. It’s a red flag in your relationship that you don’t combine your money. She went on and on about how wrong she thought it was that we were doing this. I never cared that she felt like that. Money is so personal and you should NEVER feel like you have to do something with your money just because it’s “tradition” or “what other people are doing”. This system works for Adam and I. We have no plans on changing it. It’s funny because after she said that I assumed we were the only people doing this but recently, I told three friends about how we manage our money separate and they shared that they do the same with their partner.

A snapshot of recurring expenses:

Rent

We’ve lived in the same rent stabilized one bedroom apartment for five years. Our monthly rent is around $3,400. While it might not seem like it, that’s quite the deal for the area I live in. The average one bedroom in my neighborhood is $4,300 at the moment. I pay half our rent so it comes out to $1,700 a month.

Cable & Internet

We’re not big TV watchers around here so we don’t have cable but if we did it would be $60/month. We also don’t pay for any streaming services at the moment but we do have access to a few (for now) thanks to a handful of loving friends and family members. Internet is $70/month, which is super expensive, but we use it every second of the day.

Utilities and Gas

This ranges every month but usually hovers around $250 a month. For context, our entire apartment is under 600 square feet.

Insurance

Health insurance is around $400/m and is supplemented by Adam’s employer

Pet insurance is around $40/m and is worth it for us to have

Renter’s & engagement ring insurance is bundled and comes out to $33/m

Below is a snapshot of my credit card spending categories from January-April.

It says that my most popular spending category is merchandise but that’s fake news because these charts don’t account for returns. Yes, I buy a lot of stuff but I return 90% of it. I’ve been striking out a lot lately with online shopping.

Truly, I spend way too much money on food every month. I go grocery shopping 2-3x a week and we order takeout 3-4x a week. When people talk about the cost of living being so high in NYC, they always think they are referring to rent but food is seriously so pricey here. Even at the grocery store.

When writing this week’s newsletter, I audited all of my credit card transactions from January-April. I found some ways I can be smarter with my spending.

My goal is to spend 10% less than I did last year on my credit card.

How much money I make:

This is a hard one to answer because I am en employee of my own company. I pay myself when I can. I make money in a variety of ways and the income of my business varies — so does my personal income. Rather than tell you a number, I’ll share a breakdown of all the ways I earn money every single month.

Ps. anytime you see a * next to an income stream, it means it is passive income. The TLDR is that I’ve built tools, products, or systems (marketing channels, etc.) that have the ability to earn recurring revenue without requiring much of my attention or time. This is so helpful right now in life because I’m only able to work 15-20 hours a week and spend the rest of my time with Gemma (the baby). Pre-baby, I worked 50-80 hours a week. So much of my work requires my time, skills, and attention. Before the passive income streams, I only made money when I worked more hours. I’m earning less now than I did pre-baby and trying to build up those passive income streams so that I don’t have to trade hours for .

My business: Bridesmaid for Hire

Here are the ways the business makes money:

Affiliate revenue*

Brand deals (social media, newsletter, etc.)

Google ads*

My personal brand: Jen Glantz

Paid newsletter subscribers* (thank you for supporting <3)

Brand deals (social media, newsletter, etc.)

Affiliate revenue*

Speaking (companies, conferences, universities, non-profits)

Freelance writing

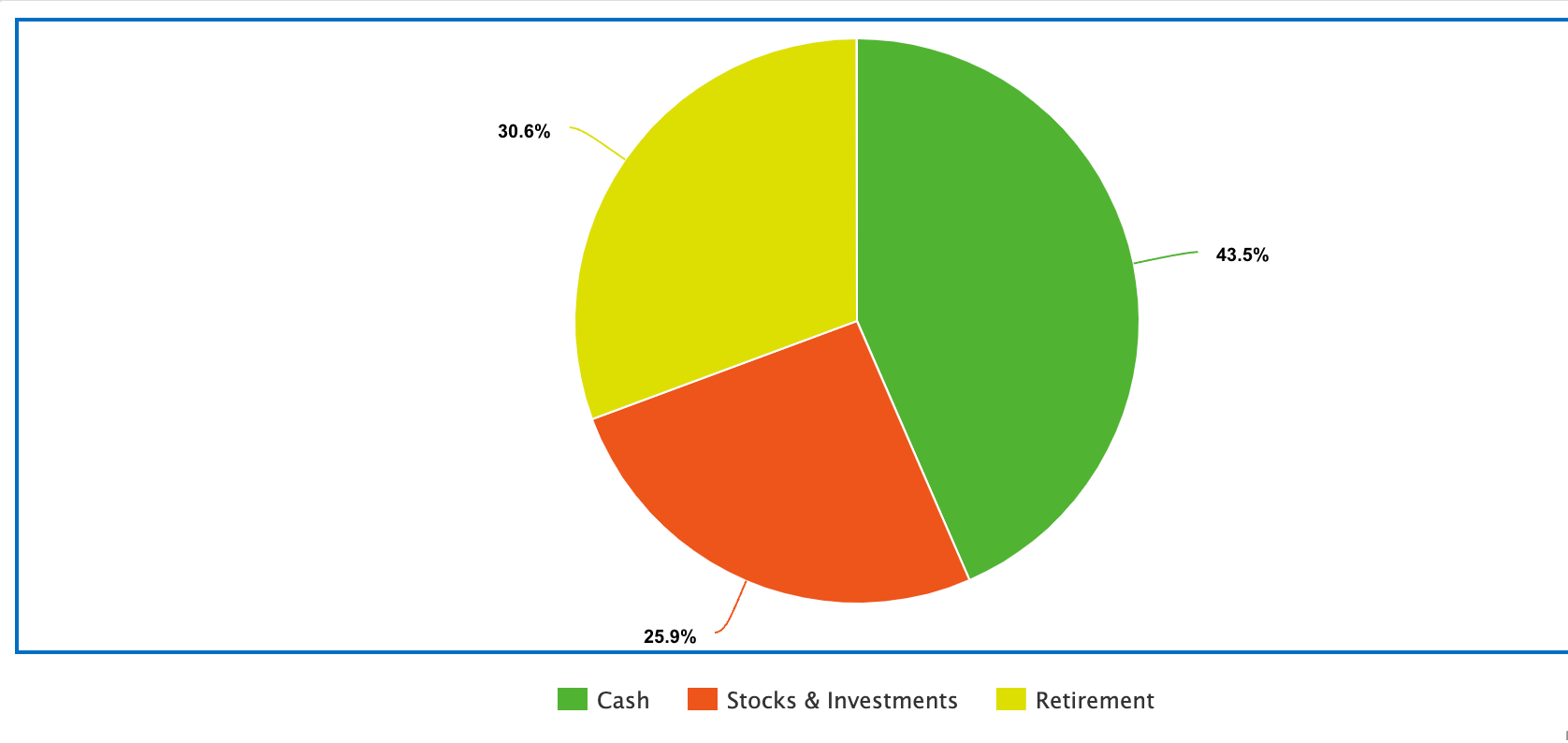

How I manage my money

None of this is financial advice! I’m not a finance expert. I’m just someone who really enjoys learning about personal finance. Also, the breakdown of where all of my money is right now isn’t something I suggest you follow. It’s a work in progress. Right now, I’m comfortable with my breakdown but I have ideas of how I want to move things around. So please do your own research, don’t follow what I’m doing because it might not be right for you, and always do what is right for you when it comes with managing your money.

Yes, I keep almost half of my money in cash. That might seem like a big mistake. Maybe it is. But for now, I’m comfortable with this strategy. Plus, all of the cash is in high-yield savings accounts earning around 4% interest (APY)or in CDs earning 5% interest (APY).

I didn’t start saving for retirement until I was in my late twenties. I have an IRA and contribute a few hundred dollars a month during the year and then another lump sum contribution at the end of the year based on my earnings.

I started investing money in the market (individual stocks, mutual funds/index funds, etc.) a few years ago. The biggest mistake I made was investing in individual stocks during the pandemic. I had no idea what I was doing and lost money this way. I also sold 98% of the cryptocurrency I bought during the pandemic as well.

Phew, okay. There ya go. My finances! Sharing this wasn’t too scary. It actually helped me make a to-do list of things I want to fix, change, and look into before the end of the year. Thanks for reading all of this. What do you think? What’s new with your finances?

⚡Instant Pick Me Ups

📚: I started this book over the weekend. Such an interesting read.

🎵: This song really turns me into a happy person who feels like she’s back on the dance floor.

💄: Beyond in love with this fun lipstick. I bought it when I was in Nashville and have been wearing it nonstop. It feels nice on my lips, has a little sparkle, and is small enough that it fits in my pocket or mini purse.

👗: A long list of recommendations for anyone attending a special event in the next few months (from dresses to shoes, gift ideas, and inexpensive jewels that look $$$).

😮 Progress Report:

Last week I shared that I was going to delete email off my phone for a week. I tried and failed. By Monday at 11am, it was back on. Change doesn’t happen overnight, my friends. I’ll try again this week.

I had to take Goofy (the dog) to see a specialist for a knee issue she is having and the doc is located inside of a big, giant animal hospital and emergency room in Manhattan. Sitting in the waiting room was so heartbreaking that I couldn’t stop crying. There’s something so terribly painful about watching animals in pain. To get my mind off it all, I paced around the waiting room. I stood close to the front desk. I watched so many people check out and heard that they were getting charged thousands, and thousands, and thousands of dollars. One guy just stood there with his lovable dog as the woman behind the desk told him that he owed $3,600 today and the other 50% after the dog’s surgery. He mentioned that he had to open up a credit card to pay for this and go into debt. I told Adam that if I ever made a lot of money, I want to pay people’s animal hospital bills. I’d just stand outside this place and hang people wads of cash as they walk in heartbroken about their pets. But saying that is a cop out because I can take action now. I’m looking into nonprofits that pay people’s vet pills. If you know any that are legit, please send them my way. When I find one that I’ve vetted, I’ll share it with you too.

Why you’re getting this: I'm Jen Glantz and this is The Monday Pick-Me-Up newsletter. I've been sending it every Monday, for 9-years, to thousands of awesome humans, just like you. Thank you for letting this email live in your inbox. It truly makes my heart explode with joy.

Become a paid subscriber: I’m building a community here with private Zoom hang-outs, workshop, bonus content, and more! Join the community and support the newsletter by becoming a paid subscriber in 2024 for $5 a month. Thank you so much for considering :)

If you liked reading this, click the ❤️ button on this post so more people can discover it on Substack!

I so agree with you that managing money is not one size fits all and there is no e.g. "right" way to split finances with your partner. Thanks for sharing this, I'm always a big fan of learning how different people budget/spend/earn/save and this was really fun to read!

Thanks for writing about your finances! I wanted to let you know you are not alone. My girlfriend and I keep our bank accounts separate but venmo each other all the time. Because I make more money than she does, we actually split things based on percentages not, "I pay half and she pays half." We do a 40/60 split. I actually love talking about money and writing things down. She doesn't. I am very proud of my credit score, I love investing! I follow/listen to people like Dave Ramsey, Suzie Orman, John Bogle, Warren Buffett and websites like The motley fool.

I really try to invest with companies that have been around forever, and companies that pay dividends. Long-term investments. I am self-taught, so I agree that everyone has to do money the way that makes them feel comfortable. I may not be 100% right either. But I love learning about it and watching my investments grow.